Shipbuilding: The long cycle of decades is finally about to start?

1. Delivery peak is approaching plate from the perspective of historical development.

The shipbuilding industry is a typical long-cycle industry. Since 1986,

the global shipbuilding industry has experienced nearly 10 large and small cycles. The bottom of the ship delivery volume moved up, and the cycle gradually shortened. The previous two rounds of downward cycles lasted 20 years and 15 years respectively.

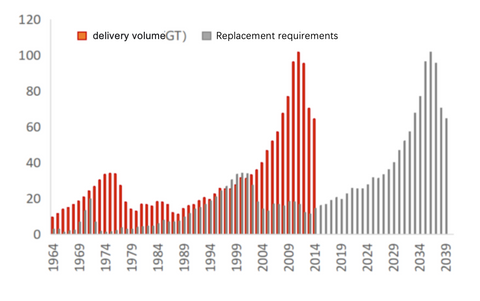

New orders for ships are a leading indicator of delivery volume. It has been nearly 12 years since the latest high ship delivery volume in 2011, corresponding to the rising cycle from 1988 to 2010, which lasted for 22 years. According to data from Wind and Clarksons, global shipbuilding completions in 2021 will be 86.02 million deadweight tons, a 46% drop from the 2011 high of 158.91 million deadweight tons, and deliveries have basically stabilized in recent years.

The China Shipbuilding Industry Association predicts that the global delivery volume in 2022 will be around 90 million deadweight tons.

Therefore, in terms of ship delivery volume, institutions have predicted that it may be close to the bottom of the current downward cycle. Previously, in March 2006, when the global new orders reached their peak, it was in January 2011 that the global ship delivery volume reached its peak, with an interval of nearly 5 years.

The second round of rising orders for new ships reached its peak in December 2013, and the total amount of ship deliveries reached its peak in January 2017, with an interval of about 3 years, which has been shortened. The latest peak of new orders for ships occurred in March 2021. Based on the 3-5 years of new orders leading delivery, the latest peak of ship deliveries may be in 2024-2026, and the recovery of industry-wide profitability is expected to be faster.

2. The aging trend of ships is obvious Steady demand for replacement Judging from the current ship age structure.

The demand for replacement will continue to rise for a long time. According to my country's "Opinions on Implementing the Compulsory Scrapping System for Transport Ships", among seagoing ships, oil tankers, bulk carriers, and general cargo ships are scrapped for 31 years, 33 years, and 34 years (inclusive) respectively.

However, according to the data from the Ministry of Communications, from 2014 to 2021, the early withdrawal of coastal bulk carriers and oil tankers in my country accounted for 96-100% and 84-100% of the total number of withdrawals in that year, respectively, and only a very small number of them were forced to scrap and exit. Therefore, The actual scrapping cycle of major ship types in my country should be less than 30 years. According to The Blue Expanse, although the longest service life of a ship can reach 30-50 years, it is difficult to maintain the service life of a ship at this level without continuous maintenance, repair and modification. The average life of a ship is 20 years -25 years.

At present, the age of oil tankers and bulk carriers continues to rise,

which is bringing new demand. According to the data of Huajing Industry Research Institute, in 2022, the shipping capacity of ships aged 16-20 years will account for 16.5%, and the shipping capacity of ships over 20 years old will account for 7.1%. The trend of ship aging is obvious. From the perspective of the average age of the three major ship types along my country's coast, the average age of oil tankers and container ships has continued to rise since 2015, and the current shipbuilding industry is in an upward cycle of renewal and replacement. Global Ship Renewal Demand and Total Delivery Forecast (Million GT) Data Source: Lloyd's Register of Shipping, Clarksons

3. Environmental protection policy intensifies Will speed up the pace of updates.

The pressure on environmental protection policies is accelerating the process of updating old ships. Shipping companies, which currently account for 2.5 percent of global carbon emissions, are under increasing pressure to reduce air and ocean pollution.

The International Maritime Organization (IMO) proposed a carbon emission reduction action plan for the shipping industry,

with the goal of reducing carbon emissions by 50% by 2050. The three short-term measures, the energy efficiency index (EEDI) for newbuildings, will be implemented in three stages starting from 2013 , the existing ship energy efficiency index (EEXI), carbon intensity index (CII) will come into effect in 2023.

CII is the carbon emission per ton per nautical mile, and the lower the CII value, the better. Calculate the emissions of carbon dioxide gas produced by ships per nautical mile in a year, and set the operating efficiency of the world's shipping fleet in 2019 as the baseline standard, which will be reduced every year thereafter. In 2023, it will be reduced by 5%, and the energy efficiency of ships will increase by 5% compared with 2019, by 7% in 2024, and by 11% in 2026.

According to the China Classification Society,

the existing capacity does not meet the requirements of EEXI, and oil tankers, bulk carriers, and container ships that need to be updated account for 70%, 77%, and 65% respectively, which will greatly catalyze the demand for ship renewal.

4. Which type of ship has the most stable demand?

Ships can generally be divided into two categories: military ships and civilian ships.

Civilian ships are usually further divided into offshore engineering ships, transport ships, etc. according to their uses, among which transport ships occupy the main position. In terms of deadweight tonnage, the total deadweight tonnage of dry bulk carriers, oil tankers, and container ships, which are all transport ships, accounts for nearly 90% of the total, making them the three major ship types in the world. In 2021, among the global ships, oil tankers will account for 29% of the shipping capacity, bulk carriers will account for 43%, container ships will account for 13%, and general cargo ships and other ships will account for 15%.

Data source: Huajing Industrial Research Institute, UNCTAD, Clarksons At present,

the global mainstream ship structure is gradually shifting from the three major ship types of bulk carriers, oil tankers and container ships to five major ship types of bulk carriers, container ships, oil tankers, LNG carriers and passenger ships. The agency believes that the current growth trend of LNG ships is still certain. From the perspective of new orders, the value of new global LNG ship orders has increased quarter by quarter from the first quarter of 2021, and the global order value in 2021 will reach 17.53 billion US dollars. In the first three quarters of 2022, the global LNG order value has reached 28.706 billion US dollars. 10 billion more than in 2021.

Due to the shortage of transit natural gas supply in Ukraine due to the conflict between Russia and Ukraine,

in the short term, LNG can only be transported by sea to supplement the European gap. The United States and the reduction are the LNG suppliers that Europe has reduced, and the reduction has filled long-term supply contracts with other Asian countries, and most of the supply has been locked. The EU's import of LNG from the United States will lead to a surge in LNG shipping volume, and Europe is expected to increase opportunities Build a large number of LNG ships to ensure the stability of natural gas imports.

According to the China Water Transport Report and Clarkson data, judging from the existing orders,

it is estimated that by 2025, Quanfuqiu will deliver 200 LNG ships (the current inventory is 691 ships), and the total capacity will increase by 1,700 tons. In terms of container ships, due to the substantial increase in container ship orders driven by the recovery of trade in the later stage, the delivery volume on the supply side increased sluggishly, and the orders in hand remained at the same level. However, the current container freight price has fallen back to the pre-epidemic level, the port is blocked, the capacity is released, and the price and order of container shipbuilding will return to rationality. In terms of oil tankers, the low rents and high ship prices in 2020-2021 have attracted the investment enthusiasm of shipowners, but the recent Russia-Ukraine conflict has changed the global crude oil trade routes, China's recent optimization of epidemic prevention and control measures, and the support of high terminals and , so that the market demand for oil transportation has been improved.

As for bulk carriers, due to the high and overvalued commodity prices in the past two years,

the dry bulk market has been greatly affected. In addition, the current container freight rate has declined, causing some cargo to flow into the container market from the dry bulk market. In the long run, the bulk carrier market is still full of uncertainties.

5. As the world's largest shipbuilding country Chinese shipping companies are expected to continue to benefit.

The shipbuilding industry is located in the middle reaches of the entire industrial chain, including marine supporting equipment, shipyards, shipbreaking yards, etc. The upstream is the raw materials required for the production of ships, such as shipbuilding plates, paints, cables, etc., and the downstream is the shipping industry that undertakes maritime transportation trade.

At present, in the field of ship design, there are CSSC and Tianhai Defense; in the field of outfitting equipment, there are Yaxing Anchor Chain, Guorui Technology, Weichai Heavy Machinery, Highlander, and China Heavy Industry; in the field of shipbuilding, there are CSSC Defense, China Shipbuilding, and Tianhai Defense, China Heavy Industry; power system field includes Weichai Heavy Machinery and China Dynamics.

Source: Wind, Guohai Securities Research Institute From the perspective of shipbuilding indicators,

the world's top three shipbuilding countries are China, South Korea, and Japan, accounting for about 5, 3, and 1 market shares. According to the data of the China Shipbuilding Industry Association, in 2021, the world's shipbuilding completions will be 33.56 million revised gross tons, new orders will be 46.96 million revised gross tons, and orders in hand will be 77.7 million revised gross tons.

The Chinese market shares will reach 41%, 49% and 48%. Among them, China Shipbuilding is one of the flagship listed shipbuilding companies with the largest scale, the most advanced technology and the most complete product structure in China. It has obvious advantages in technology brand, business scale and synergy, and product structure. The company's main business is shipbuilding, ship repairing, and machine building, and has also developed non-shipping businesses such as marine engineering and electromechanical equipment.

In 2021, CSSC's total orders, container ships, and bulk carrier orders will all rank first in the world. According to the statistics disclosed in the company's annual report announcement, in the whole year of 2021, the company has undertaken orders for 132 ships with a deadweight of 12.1117 million tons, and the tonnage has completed 164.37% of the annual plan, accounting for 9.72% of the global total.

At present, China Shipbuilding is also leading the industry to move towards high value-added ship types.

Founded in 1981, Yaxing Anchor Chain has successively broken foreign monopoly in subdivided fields such as marine, marine engineering, sea breeze, and mining for more than 40 years, and has become the leader in the global chain industry.

In the field of marine anchor chains, the company's products have passed the certification of many international classification societies, which are the safety guarantee for ship navigation; in the field of mooring chains, the products have completed six update iterations, and successfully independently developed the world's highest-level R6 Mooring chain, superior performance.

Tianhai Defense, the largest private ship design company,

has also gradually grown into a characteristic enterprise integrating ship and sea engineering, defense equipment, and new energy. Although the company encountered a cash liquidity crisis at the bottom of the 2018 cycle, in 2020, Longhai Zhongneng and others intervened in the company's operations and invested more than one billion yuan in business restructuring.

At the beginning of 2021,

the company actively introduced technical personnel in the fields of defense, energy, and finance, completed the change of senior management such as the board of directors, and maintained the stability of the core management, finance, and technical teams.

After optimizing the reorganization of shareholders and governance structure,

the cash flow of operating activities has improved significantly, and the reorganization has achieved initial results. The company is also the only comprehensive solution provider integrating ship design and construction in the shipbuilding industry chain. The above domestic shipbuilding related companies are expected to enjoy the long-term dividends brought about by the start of the big cycle.

If you have the following requirements: New ship manufacturing/ Second-hand ships trading/ Ship quality assessment/ Equipment maintenance/ Connecting Chinese ship brokers/ Third-party ship transaction guarantees service.

Contact: contact@vesselslink.com